Solid Finish to FY ’22 But FY ’23 Comes-Out Craps; Lowering Price Target to $9.50

DHI Group’s (DHX) Q4 ’22 results exceeded expectations for the most part, except for bookings, which unfortunately is what matters most. Revenue again outpaced our estimates and consensus, which in turn drove another adjusted EBITDA beat to end the year. Although revenue retention rates remained strong across both Dice and ClearanceJobs, new business bookings for the former were impacted by elongated sales cycles as customers paused to reassess hiring plans amid an uncertain economic backdrop. As a result, Dice bookings declined slightly from the year-ago period, marking a significant deceleration from the mid-teens growth last quarter and the loftier levels seen earlier in FY ’22. On a more positive note, ClearanceJobs remains unaffected by the macro environment thus far, and may well be deemed recession-proof given the record defense budget approved at the end of last year.

Reflecting the softness in Dice bookings entering the new year, management guided for low double-digit revenue growth in FY ’23 and an adjusted EBITDA margin at or near 20% with expansion anticipated during the latter half of the year. While the margin target remains consistent with our prior expectations, the revenue outlook represents a guide-down of sorts from management’s commentary during its September investor day, which suggested that both bookings and revenue growth could remain near 20% in 2023. Of course, much has changed since then, including signs that the economy is softening and tight labor market conditions may finally be easing. With this context, guidance for double-digit revenue and bookings growth is nothing to scoff at, in our opinion, especially given management’s penchant for conservatism.

We lower our estimates for this year and next, primarily reflecting a near-term deceleration in Dice bookings. Worth noting, our model assumes a recovery in Dice bookings beginning in Q2 ’23 with a return to growth rates in the mid- to high-teens by year-end. Our optimism is underpinned by the tech unemployment rate falling to 1.5% in January and an increase in job postings for future tech hiring that reversed a dip in December, according to analysis by CompTIA. We surmise that so long as demand for technology talent remains high and the supply of said talent remains low, opportunities for Dice will ultimately move forward. In the interim, our price target declines from $10.50 to $9.50 as we apply an unchanged FY ’23 EV/Sales multiple of 3x to our lower estimates. We continue to believe shares are undervalued and see several potential near-term catalysts, including a rebound in Dice bookings later this year and an expansion in the company’s buyback program upon the expiration of the current authorization this month.

Exhibit I: Reported Results and Guidance Versus Expectations

Sources: DHI Group; K. Liu & Company LLC; FactSet Estimates

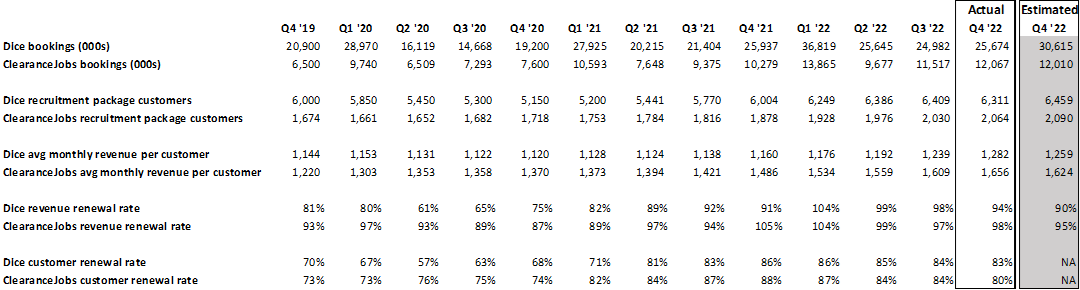

Q4 revenues of $39.8 million (+17.8% Y/Y) exceeded management’s guidance of $38.5-$39.5 million, our estimate of $39.0 million and consensus of $38.9 million. Both Dice revenues of $28.2 million (+15.6% Y/Y) and ClearanceJobs revenues of $11.6 million (+23.5% Y/Y) surpassed our estimates of $28.0 million and $11.0 million, respectively. Although ClearanceJobs bookings of $12.1 million (+17.4% Y/Y) were consistent with our $12.0 million projection, Dice bookings of $25.7 million (-1.0% Y/Y) were well below our $30.6 million forecast as new customer bookings were delayed by cautious buying behavior. Moreover, revenue retention rates remained strong and were ahead of our expectations, but the customer retention rate dipped slightly on a sequential and Y/Y basis, resulting in ending customer counts for both Dice and ClearanceJobs coming in below our estimates. Per management, the losses were largely limited to smaller customers generally with annual contract values below $10,000. Relative to our model, the lower customer counts were offset by higher average revenues per customer across both platforms.

Exhibit II: Key Metrics

Sources: DHI Group; K. Liu & Company LLC

Gross margin of 88.0% was 20bps above our 87.8% assumption, while total operating expenses were in line with our estimate. Reflecting the upside in revenue, adjusted EBITDA of $8.1 million (20.4% margin) beat our estimate of $7.3 million and consensus of $7.7 million. EPS of $0.05 beat our estimate of breakeven and consensus of $0.01 due to the upside in operational results as well as $2.1 million in proceeds from a litigation settlement.

Cash at the end of Q4 totaled $3.0 million, while debt outstanding remained unchanged at $30.0 million. In Q4, DHI Group generated $7.3 million in cash from operations, used $4.6 million for capital expenditures and repurchased approximately 640,000 shares for $3.6 million, or an average price of $5.59 per share.

For FY ‘23, management’s initial guidance calls for low double-digit revenue growth, implying revenues of $164.6-$167.6 million. Prior to revisions, we were projecting $173.8 million in revenues while consensus was at $172.8 million. Guidance also assumes DHI Group maintains an adjusted EBITDA margin at or near 20%, implying adjusted EBITDA of $32.9-$33.5 million versus our previous $38.8 million estimate and the Street’s $37.0 million. We note that the low double-digit revenue growth rate is expected in each quarter of the year, and the adjusted EBITDA margin is expected to expand in the next six to twelve months.

Exhibit III: Estimate Revisions

Source: K. Liu & Company LLC

We reduce our revenue estimates for this year and next based on more conservative assumptions for Dice bookings growth. We now expect Dice bookings growth in the low double-digit range versus the mid-teens previously. Although the revenue haircut was slightly offset by a modest decline in our operating expense assumptions, our adjusted EBITDA estimates also fall in concert. We note that our EPS estimates also decline due to the combined impacts of lower adjusted EBITDA and higher interest expenses.

Our report with model and disclosures is available here.

Disclosure(s):

K. Liu & Company LLC (“the firm”) receives or intends to seek compensation from the companies covered in its research reports. The firm has received compensation from DHI Group, Inc. (DHX) in the past 12 months for “Sponsored Research.”

Sponsored Research produced by the firm is paid for by the subject company in the form of an initial retainer and a recurring monthly fee. The analysis and recommendations in our Sponsored Research reports are derived from the same process and methodologies utilized in all of our research reports whether sponsored or not. The subject company does not review any aspect of our Sponsored Research reports prior to publication.