Initiating Coverage of DHI Group

We are initiating coverage of DHI Group, Inc. (DHX) with a price target of $8.00, representing a FY ’22 EV/Sales multiple of 3x. Amid the recovery from the COVID-19 pandemic, “The Great Resignation” has created new challenges as businesses struggle to fill a growing number of open positions. We believe this backdrop provides a favorable tailwind for DHI Group, which has divested several non-core assets in recent years and is now squarely focused on operating two highly regarded technology career marketplaces, Dice and ClearanceJobs. Between the evolution of the Dice platform from a job board to a two-sided career marketplace and significant investments in sales and marketing, we expect sustained double-digit growth going forward along with more material margin expansion over the long-term. The improved fundamentals are already evident as DHI Group returned to positive revenue growth in Q2 ’21 and saw further acceleration in Q3 ’21 driven by robust growth in bookings and subscribers across both of its core platforms. With shares trading at just over 2x our FY ’22 revenue estimate and 11x projected EBITDA versus the peer group median at 4x and 29x, respectively, we believe the market has overlooked DHI Group’s highly recurring revenues, the successful turnaround in its Dice business and its strong cash flow generation.

Investment Highlights

Dice At an Inflection Point. In late 2016, DHI Group announced a new tech-focused strategy, which signaled the start of several non-core asset sales and the search for a new leader. Subsequently, Art Zeile joined as CEO in April 2018 with a mandate to guide the company through its tech-focused strategy and return the business to growth. With Dice comprising over 80% of sales but shedding 10% of its revenues at the time, stemming the decline and returning Dice to growth was of utmost importance. Step one was to upgrade the user experience, which included enhancing search functionality, improving candidate quality by reducing the number of fake profiles, and introducing communication features enabling recruiters and candidates to engage on the platform. Step two was refining the sales strategy to focus on commercial accounts, specifically medium to large businesses targeting ten or more hires, and adding new business reps to target the expanded customer set. In this regard, the number of reps focused on new business has increased by 5x over last three years and by 20% this past year. Finally, new leadership was put in place in the marketing organization and significant investments made in digital marketing, resulting in a 20-fold increase in marketing qualified leads. These initiatives are now bearing fruit with Dice bookings +46% Y/Y, revenue +12% Y/Y and recruitment package customers +9% Y/Y in Q3 ‘21. The turnaround at Dice also coincides with management’s outlook for revenue growth to approach 20% in the current quarter.

A Hidden Gem. ClearanceJobs is a highly differentiated online career marketplace for professionals with security clearances. Over the past five years, ClearanceJobs has grown at a CAGR of 20%, and we believe the platform can sustain a growth rate of 15% to 20% for the foreseeable future. Although growth has historically been driven by adoption among government contractors, management sees incremental opportunities arising from selling directly to the hundreds of U.S. government agencies that compete with enterprises for technology talent. Worth noting, the federal government comprised less than 1% of revenue prior to Art Zeile’s appointment as CEO, and there are now 30 active engagements underway that could contribute more meaningfully in the years to come. Aside from boosting revenue growth, ClearanceJobs also serves as a test bed for innovation as features that resonate on the platform ultimately find their way over to Dice. Given its consistent track record of growth, strong retention rates and unique talent pool, we believe ClearanceJobs would garner a premium valuation in its own right.

Large Addressable Market. We estimate DHI Group’s serviceable available market at approximately $1.5 billion based on management’s statements indicating there are approximately 18,000 staffing and recruiting firms and another 80,000 commercial accounts that are in Dice’s sweet spot, as well as 10,000 defense contractors targeted by ClearanceJobs. In deriving our projection, we assume average monthly revenue per Dice and ClearanceJobs customer of $1,138 and $1,421, respectively, matching the levels reported in Q3 ’21.

High Mix of Recurring Revenues. Over 90% of DHI Group’s revenue is derived from sales of recruitment packages for the Dice and ClearanceJobs platforms. These packages start at a list price of $7,000 per recruiter per year, typically with a one-year term and increasingly with built-in auto-renewal clauses providing for a 9% uplift in pricing. Importantly, revenue renewal rates have consistently exceeded 90% for ClearanceJobs and have improved meaningfully for Dice, which also recently crossed the 90% threshold. The remaining non-recurring revenue arises from ancillary services such as advertising, corporate branding and sourcing.

Profitable and Cash Flow Generative. Even amid revenue declines and investments to enhance the Dice platform in recent years, DHI Group’s adjusted EBITDA margin has generally hovered around 20%. While ongoing investments to ramp sales headcount and support digital marketing initiatives are likely to limit margin expansion in the near-term, management anticipates maintaining an adjusted EBITDA margin of at least 20% moving forward and sees potential for that to approach 30% within the next three years. Of course, the strong operating leverage translates into solid free cash flow generation, which has primarily been used for share repurchases. At the end of Q3 ’21, DHI Group’s existing buyback program had a remaining authorization of $11 million.

Optionality via Strategic Investments. Although much of DHI Group’s tech-focused strategy resulted in the sale of non-core assets, there have been some instances in which a majority ownership was transferred to existing management with DHI Group maintaining a minority interest in the standalone entities. These holdings include a 20% stake in BioSpace and a 40% interest in RigZone, both of which were previously written off and are no longer carried on the balance sheet. More recently, the transfer of eFinancialCareers to its management team left DHI Group with a 40% interest in the business, which is currently valued at $3.6 million. Additionally, DHI Group made a $3.0 million investment in The Muse, an online corporate branding platform used by organizations to attract and hire talent, which is carried at cost on the balance sheet.

Valuation. DHX shares trade at just 2.3x and 10.9x our FY ’22 revenue and adjusted EBITDA estimates, respectively, a significant discount to the median multiples afforded to both its online recruiting and human capital management (HCM) software comps. We note that the online recruiting peer group trades at median FY ‘22 EV/Sales and EV/EBITDA multiples of 4.1x and 29x, respectively, while the median multiples across the HCM software space are even higher at 14x forward sales and nearly 63x adjusted EBITDA. Our price target of $8.00 represents a FY ’22 EV/Sales multiple of 3x and an EV/EBITDA multiple of 15x. Although a higher valuation is certainly achievable, we believe a discount to the online recruiting group median is appropriate at this juncture given DHI Group’s current scale and its relatively recent return to revenue growth. In other words, should the company demonstrate sustained growth and margin expansion over a longer time horizon, we think the stock could re-rate to levels well above our current price target.

Investment Risks

Acquisitions. Although DHI Group has primarily been divesting assets in recent years, management actively evaluates potential acquisitions. As such, the company could overpay for an acquisition, face significant integration issues, or fail to realize expected synergies, which in turn could lead to earnings dilution and other negative outcomes.

Competition. The market for talent acquisition services is highly competitive and includes both traditional staffing firms, online job boards and other internet-based recruiting platforms targeted at specific niches. Among others, DHI Group competes with job listing aggregators such as Recruit Holdings Co.’s Indeed and ZipRecruiter, social and professional networking sites such as Microsoft’s LinkedIn and Facebook, general job boards including CareerBuilder and Monster.com, and freelance marketplaces such as Upwork.

Debt. At the end of Q3 ’21, DHI Group had $17.7 million in debt outstanding under a $90.0 million revolving loan facility. Borrowings under the revolver bear interest, at the company’s option, at LIBOR plus 1.75% to 2.50% or a base rate plus 0.75% to 1.50%, depending upon its most recent consolidated leverage ratio. Although we believe the company’s debt load is manageable, an inability to service its obligations could significantly impair the company’s financial position and its ability to fund its operations.

Economic Conditions. Demand for the company’s services is subject to labor market conditions and may be negatively impacted by any slowdown in recruitment activity arising from economic and business cycles.

Intellectual Property. DHI Group depends on its intellectual property, including its internally developed technology, the content on its websites and its trademarks, to compete. An inability to protect its intellectually property against infringement or other misuse could adversely affect the company’s business.

Missed Expectations. Although much of its revenue is recurring in nature, the company could miss its own guidance or consensus estimates, which in turn could cause a decline in shares of DHX.

User Privacy and Other Government Regulations. DHI Group collects and stores information about both professionals and customers on its platforms. Although much of the data is provided by these parties with the intent to make it publicly available, violations of its own privacy policy or other government regulations related to its online services, advertising and data protection could have a negative impact on the business.

Company History

DHI Group’s origins date back to 1990 when Data Processing Independent Consultants Exchange, aka DICE, was founded by Lloyd Linn and Diane Rickert. At the time, DICE was a bulletin board service where open jobs were listed and made accessible only to technical contractors and the recruiting, staffing and consulting firms looking to hire them. As websites became increasingly prevalent in the ensuing years, DICE moved to the world wide web and adopted the Dice.com URL in 1996. Shortly thereafter, the company was acquired by publicly traded EarthWeb, which eventually changed its name to Dice Inc. in 2001. Two years later, Dice filed for bankruptcy under Chapter 11 and was recapitalized in a go-private transaction. After emerging from bankruptcy, the company acquired ClearanceJobs in 2004 and Targeted Job Fairs the following year. In August 2005, Dice Holdings, an entity formed by private equity firms General Atlantic and Quadrangle Group, acquired Dice. Just over a year later, eFinancialGroup, the parent company of eFinancialCareers.com, eFinancialNews and JobsintheMoney.com, was acquired by Dice Holdings for £56.5 million. Dice Holdings completed its IPO in 2007 under the symbol DHX and changed its name to DHI Group in 2015.

Prior to its corporate name change in 2015, DHI Group amassed a number of online recruiting websites targeted at a specific verticals, including biotechnology, energy, healthcare and hospitality. However, revenues peaked in 2014 and after experiencing ongoing declines through the first half of 2016, the Board of Directors initiated a strategic review, including an exploration of strategic alternatives. The strategic review ultimately led to DHI Group’s tech-focused strategy, but after running a comprehensive process that generated interest from strategic and financial parties, the Board opted to remain independent. With a sale of the company off the table, the company began executing against its tech-focused strategy in earnest and initiated a search for a new CEO in 2017. Health eCareers was sold in December 2017, and majority ownership of BioSpace was transferred to its management team in January 2018. Several months later, Art Zeile joined the company as its new CEO with a mandate to execute against the tech-focused strategy and return the company to growth and improved profitability. Over the course of 2018, DHI Group divested the RigLogix portion of its RigZone business, sold its Hcareers business and transferred majority ownership of the remaining RigZone business to its management team. New leadership was also put in place for the marketing and product organizations. In 2019, the new executive team was rounded out with the additions of Kevin Bostick as Chief Financial Officer, Arie Kanofsky as Chief Revenue Officer, Paul Farnsworth as Chief Technology Officer and Chris Henderson as Chief Strategy Officer. Revenues from the remaining tech-focused segment, namely Dice, ClearanceJobs and eFinancialCareers, also stabilized and were down only modestly for the year.

Throughout 2020, DHI Group continued to invest in new product innovation, expansion of its sales and account management teams and digital marketing. Of course, the COVID-19 pandemic weighed on growth, particularly for the Dice and eFinancialCareers brands. The latter was also negatively impacted by uncertainty related to Brexit. More recently, majority ownership of eFinancialCareers was transferred to its management team at the end of June 2021 with DHI Group retaining a 40% interest currently valued at $3.6 million. In September 2021, DHI Group also announced a $3.0 million investment in The Muse, a career destination site for the next generation of workers to research companies and career opportunities. Between the shedding of non-core assets and the benefits of investments made across product, sales and marketing, DHI Group saw revenues return to positive growth in Q2 ’21 and saw that growth accelerate into the low-teens in Q3 ’21.

From Job Boards to Career Marketplaces

DHI Group operates two online career marketplaces, Dice and ClearanceJobs, enabling recruiters and hiring managers to search, match and connect with candidates possessing specific technology skills and security clearances. In general, the company’s career marketplaces enable recruiters and candidates to create profiles, post jobs and resumes, and search for relevant prospects and opportunities. With the addition of email and messaging capabilities, recruiters and candidates may also engage directly on the platforms. Moreover, DHI Group continues to introduce new capabilities like alerts and workflow automation that are moving its platforms even further away from the static job boards of the past to the dynamic, two-sided career marketplaces of the future.

Dice has long been used by technology and engineering professionals in the U.S. to post their resumes, search for jobs and access an array of career-related content, news and tools. In 2020, Dice averaged approximately 1.5 million monthly users and had approximately 58,000 job postings at year-end. The ability to find new opportunities and resources to move their careers forward attracts technologist to the website, and over 9 million candidate profiles have been created on Dice, resulting in one of the largest databases of technology talent in existence. This large candidate pool is of course attractive to recruiters and hiring managers seeking to fill open positions requiring specific technical skills. Dice’s secret sauce in serving the needs of recruiters, however, comes down to its AI-driven IntelliSearch, which allows for an entire job post to be entered in the search field, quickly matches the required skills to relevant technology professionals and rank orders the results to streamline the recruiting process. At last report, Dice now boasts 5,770 recruitment package customers representing approximately 30,000 active recruiters in its system. We note that recruitment packages are sold on a per-seat basis with a list price of $7,000 for one-year terms and comprise over 90% of Dice’s revenues. Per management, Dice’s sweet spot is companies targeting 10 or more hires and its addressable market is comprised of 18,000 recruiting and staffing agencies as well as 80,000 commercial entities. Aside from purchasing recruitment packages, customers may also opt for ancillary services such as advertising, corporate branding and sourcing, all of which generate non-recurring revenue for Dice.

ClearanceJobs is an online career network targeted at security-cleared professionals and the U.S. government contractors, federal agencies, national laboratories and universities that search for candidates with active security clearances. In 2020, ClearanceJobs averaged approximately 621,000 monthly users and exited the year with about 53,000 job postings. Over 1.3 million security-cleared professionals have been registered, which is particularly impressive as there are only 3.8 million U.S. citizens with an active security clearance. Worth noting, the number of individuals holding a security clearance includes 1.4 million active-duty military members, who are unlikely to be looking for a job, leaving just 2.4 million professionals for employers to target. Since obtaining a secret clearance currently requires about 122 days and acquiring a top secret clearance takes around 160 days, many employers tend to seek out candidates that already have a clearance. In this regard, 81% of those with a security clearance are employed, so employers often have to entice them away from their existing jobs. In our view, ClearanceJobs provides the platform to accomplish this through its large candidate pool, verified recruiter profiles, professional networking features, two-way messaging, and alerting and automated workflow capabilities. Similar to Dice, ClearanceJobs sells recruitment packages that we believe may approach as much as $10,000 per seat for a one-year term. ClearanceJobs has historically pursued the 10,000 defense contractors serving the U.S. government but is now also looking to engage directly with federal agencies. At the end of Q3 ’21, ClearanceJobs had 1,816 recruitment package customers. Given its size relative to Dice and early moves to evolve into a two-side career marketplace, ClearanceJobs also serves as a test bed for innovation, meaning features that resonate there eventually find their way into the Dice platform.

Both Dice and ClearanceJobs compete with other online recruiting platforms such as Indeed and ZipRecruiter as well as online job boards such as CareerBuilder and Monster. Competition also comes from social and professional networking sites like Facebook and LinkedIn as well as online classified websites like Craigslist. ClearanceJobs also competes with others focused on the cleared professionals space, including ClearedCareers, ClearedJobs.Net and USAJOBS, a U.S. Office of Personnel Management website used to connect job seekers with federal employment opportunities. We believe Dice and ClearanceJobs are differentiated by their respective talent databases, search and ranking algorithms, and professional networking and communication features.

Opportunity Amid The Great Resignation

Growth in the online recruiting industry is dependent in part on macroeconomic factors, including the demand for labor, level of unemployment and wage inflation. Specifically, rising labor requirements, low unemployment rates and higher wages all fuel demand for tools and services to attract workers. The shift in job listings from traditional media sources to the Internet has also contributed to robust growth in the Online Recruitment Sites industry, which IBISWorld expects to reach $13.1 billion in revenue in 2021, reflecting a five-year CAGR of 17.9%. Per IBISWorld, the healthcare vertical accounts for 40% of revenue in the Online Recruitment Sites industry, followed by manufacturing and retail at 30%. Relevant to DHI Group, the information technology vertical accounts for 6.6% of overall revenue, implying a total addressable market of $865 million. At present, Recruit Holdings Co. Ltd., parent company of Indeed and Glassdoor, is the reported market leader in the online recruiting space with $4.1 billion in revenue, or 31.2% market share, followed closely by Microsoft’s LinkedIn, which is estimated to have $4.0 billion in revenue, or a 30.3% share of the market. CareerBuilder rounds out the top three with an estimated $616.2 million in revenue, or 4.7% market share. Looking forward, IBISWorld projects revenue of $20.3 billion by 2026 for the Online Recruiting Sites industry, representing a five-year CAGR of 9.1%.

Of course, DHI Group’s addressable market opportunity is directly linked with broader trends across the technology landscape. According to CompTIA, net technology employment reached 12.2 million workers in 2020, essentially flat Y/Y, and is projected to increase 2% to 12.4 million workers in 2021. Worth noting, over 3.9 million technology jobs were posted in 2020. We note that the relative stability in technology employment throughout the COVID-19 pandemic stands in stark contrast to the broader economy as over 20 million Americans lost their jobs in April 2020 alone. However, robust demand for technology services and infrastructure to support remote work, e-commerce and other digital initiatives left unemployment rates for the technology sector well below the national rate throughout the depths of the pandemic. That trend has continued even amid the recovery from the pandemic with unemployment among technology occupations sitting at 2.6% in November 2021 versus a national average of 4.2%.

Exhibit I: U.S. Job Openings & Quits (in 000s)

Source: U.S. Bureau of Labor Statistics Job Openings and Labor Turnover Survey

One interesting dynamic that has emerged amid the recovery from the COVID-19 pandemic has been persistently high quit rates, a phenomenon dubbed “The Great Resignation.” Data from the U.S. Bureau of Labor Statistics reveals that the 4.5% resignation rate in the technology industry has been higher than in other industries. Given the already low unemployment rates among technology workers and expectations for employment in computer and IT occupations to grow 13% from 2020 to 2030, above the average for all occupations according to the U.S. Bureau of Labor Statistics’ Occupational Outlook Handbook, we believe the backdrop is favorable for DHI Group. Also worth considering, the median annual wage for computer and IT occupations was $91,250 in May 2020, considerably higher than the median annual wage of $41,950 for all occupations. As placement fees in the staffing industry are generally a percentage of a candidate’s annual salary, the return on investment for a Dice subscription is significant both for staffing firms attempting to fill roles as well as internal hiring managers hoping to reduce recruiting costs. In short, we believe “The Great Resignation” and ongoing war for talent in the technology sector will provide a tailwind to DHI Group for the foreseeable future. Between the 18,000 staffing firms and 80,000 commercial entities in Dice’s sweet spot, as well as the 10,000 defense contractors targeted by ClearanceJobs, we estimate the company’s serviceable available market at approximately $1.5 billion.

Financial Summary

Over 90% of DHI Group’s revenue is derived from sales of recruitment packages for its Dice and ClearanceJobs platforms. Recruitment packages are priced on a per-seat basis and generally have a one-year term. Recruitment package bookings are therefore recognized ratably into revenue over the term of the contract. Said differently, over 90% of DHI Group’s revenue is subscription-based and recurring in nature. Additionally, DHI Group is increasingly inserting auto-renewal clauses with built-in price increases averaging 9% into its contracts and is pushing for multi-year agreements, both of which we expect to provide an uplift to customer and revenue renewal rates in the future. The remaining revenue is transactional in nature and arises from ancillary services such as advertising, corporate branding and sourcing activities.

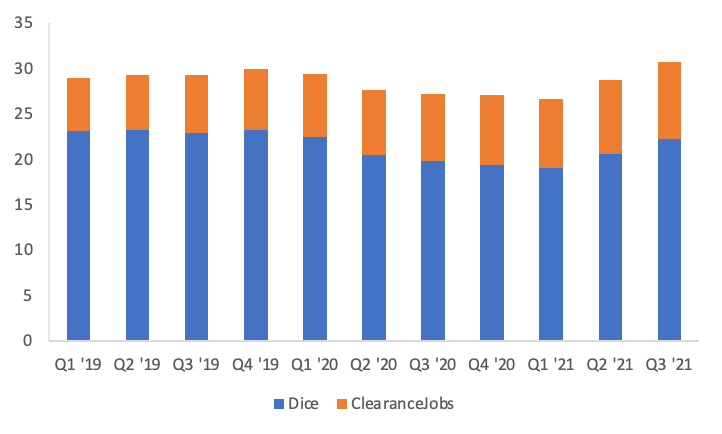

Exhibit II: DHI Group Revenues (in MMs) by Segment

Sources: DHI Group’s SEC Filings; K. Liu & Company LLC

After transferring majority ownership of eFinancialCareers to its management team in Q2 ’21, DHI Group now derives all of its revenues from Dice and ClearanceJobs. As mentioned earlier, Dice was on a downward trajectory between 2015 and 2020 due to underinvestment in product, sales and marketing, which resulted in a CAGR of (8.6)% during that period. In 2020, Dice generated revenue of $82.2 million (-11% Y/Y) and exited the year with 5,150 recruitment package customers (-14% Y/Y), average monthly revenue per recruitment package customer of $1,120 (-2% Y/Y), a revenue renewal rate of 75% and a customer renewal rate of 68%. Partially offsetting those declines was strong, sustained growth at ClearanceJobs, which posted a five-year CAGR of 20.1% between 2015 and 2020. ClearanceJobs contributed revenue of $29.0 million (+17% Y/Y) in 2020 and exited the year with 1,718 recruitment package customers (+3% Y/Y), average monthly revenue per recruitment package customer of $1,370 (+12% Y/Y), a revenue renewal rate of 87% and a customer renewal rate of 74%. Given that incremental costs to serve new recruiting package customers are nominal, DHI Group boasts a strong gross margin profile, which has remained in the mid-80% range throughout CEO Art Zeile’s tenure. This in turn has yielded strong adjusted EBITDA margin, which has generally hovered around 20% since 2018.

Exhibit III: Dice and ClearanceJobs Key Performance Indicators

Sources: DHI Group’s SEC Filings; K. Liu & Company LLC

Thus far in FY ‘21, Dice has exhibited steady improvement with revenues stabilizing in Q2 and growth accelerating to 12.4% in Q3. ClearanceJobs also remains on a strong growth trajectory with revenue increasing 14.5% Y/Y and 15.8% Y/Y in Q2 and Q3, respectively. In total, DHI Group generated revenue of $30.8 million (+13.3% Y/Y), adjusted EBITDA of $6.4 million (20.7% margin) and non-GAAP EPS of $0.05 in Q3 ’21. Dice accounted for $22.3 million of revenue in Q3, while ClearanceJobs comprised the remaining $8.5 million. Dice exited Q3 with 5,770 recruitment package customers (+9% Y/Y), average monthly revenue per recruitment package customer of $1,138 (+1% Y/Y), a revenue renewal rate of 92% and a customer renewal rate of 83%. Clearance Jobs exited Q3 with 1,816 recruitment package customers (+8% Y/Y), average monthly revenue per recruitment package customer of $1,421 (+5% Y/Y), a revenue renewal rate of 94% and a customer renewal rate of 87%. Although no formal guidance was provided, management indicated that revenue growth in Q4 could approach 20%, implying revenue near $32.4 million, and adjusted EBITDA margin should remain at or near 20%. Beyond Q4, management has previously suggested that DHI Group is capable of sustaining double-digit revenue growth, and as the company continues to scale, adjusted EBITDA could reach the high-20% or 30% level within two to three years.

Exhibit IV: DHI Group Estimates

Sources: K. Liu & Company LLC; IBES Estimates

For Q4, we project revenue of $31.9 million (+18.0% Y/Y). Our estimate reflects Dice revenue of $23.1 million (+19.0% Y/Y) and ClearanceJobs revenue of $8.8 million (+15.4% Y/Y). We expect gross margin to remain relatively consistent with recent quarters at 87.5% and have modeled a sequential uptick in operating expenses, resulting in adjusted EBITDA of $6.6 million (20.8% margin). Beyond 2021, we expect Dice to sustain a growth rate in the low double-digit range and project ClearanceJobs growth in the mid-teens. Although we see potential for significant operating leverage over time, we assume the strong growth anticipated in the near-term will prompt further reinvestment in sales and marketing. As such, we have modeled only modest adjusted EBITDA margin expansion through 2023. Specifically, our estimates for 2022 include a 12.6% Y/Y increase in revenue to $132.9 million and adjusted EBITDA of $27.9 million (21.0% margin), while our estimates for 2023 call for revenue of $150.1 million (+12.9% Y/Y) and adjusted EBITDA of $33.1 million (22.1% margin). We note that our non-GAAP EPS estimates may not be comparable to the current consensus forecast as there appears to be a mix of GAAP and non-GAAP estimates in consensus.

Valuation

Shares of DHX currently trade at just 2.3x and 10.9x our FY ’22 revenue and adjusted EBITDA estimates, respectively. We believe DHI Group’s closest peers include online job boards, recruiting platforms, career marketplaces and other professional networks. Unfortunately, the most notable brands in these categories have largely been acquired by traditional staffing firms, which have dramatically different recurring revenue and margin profiles and tend to trade at lower valuations. Still, we have included the parent companies of Hired, Monster Worldwide, and Indeed within our online recruiting comps for reference, and have rounded out the group with ZipRecruiter (ZIP) and several publicly traded freelance marketplaces. Given the disparity in business models and valuations, we think the group median, which reflects FY ’22 EV/Sales and EV/EBITDA multiples of 4.1x and 28.8x, respectively, is a more appropriate reference point than the mean. Incidentally, the median multiples are also relatively consistent with those of ZipRecruiter and Recruit Holdings Co. Ltd. (parent company of Indeed and Glassdoor), which we consider the most appropriate comps at present. As both companies have greater scale and a longer track record of growth, we surmise a slight discount to their valuations may be warranted for the time being. That said, if DHI Group’s recent growth rates prove sustainable, then a multiple in line and perhaps even higher than the group median is certainly plausible.

Exhibit V: Online Recruiting Comps

Sources: Company Filings; IBES Estimates; K. Liu & Company LLC

As the online recruiting group is rife with companies that tend to be more reliant on transactional revenue, we also considered the Human Capital Management (HCM) software vendors in our peer group analysis. We note that these vendors typically offer a recruiting module within their broader application suites, boast significant levels of recurring revenue and have a similar gross margin profile to DHI Group. In this regard, DHI Group’s business model is arguably more comparable to those in the HCM software camp than those in our online recruiting group. The primary differences, in our view, are the greater upsell opportunities available to the HCM software vendors, which typically report net revenue retention rates well in excess of 100%, and the scale at which many are continuing to post strong growth. These qualities in turn translate into lofty valuations across the group. Although we are not yet arguing for a similar multiple, we think a case could be made that DHX shares could one day trade a bit closer to these peers.

Sources: Company Filings; IBES Estimates; K. Liu & Company LLC

Given the considerable consolidation that has occurred in the online recruiting space, we believe a review of precedent transactions also provides helpful context regarding an appropriate valuation range for DHX shares. Although far smaller in scale, we note that both Dice and ClearanceJobs boast a significant number of user created profiles, offer subscription-based plans on a per-seat basis and have embedded professional networking, news feeds and messaging capabilities, all of which are very reminiscent of LinkedIn. Recall that Microsoft acquired LinkedIn in 2016 for $26.2 billion, which represented TTM revenue and adjusted EBITDA multiples of 8.2x and 40x, respectively. Also in 2016 but on the other end of the valuation spectrum, Randstad acquired Monster Worldwide for an enterprise value of $429 million, equating to TTM EV/Sales and EV/EBITDA multiples of just 0.7x and 4.9x. We note that Monster Worldwide’s revenue and adjusted EBITDA were both declining at the time, so we view the depressed multiples as an indicator for where DHX shares could trade if the turnaround goes awry.

More recently, Recruit Holdings Co. Ltd. acquired Glassdoor in 2018 for $1.2 billion, representing a TTM EV/Sales multiple of 7.3x. Also in 2018, Adecco acquired Vettery, an online recruiting marketplace with an emphasis on technology hires. Although terms of the transaction were not disclosed, media reports suggested that Adecco paid over $100 million. Interestingly, Vettery had onboarded approximately 10,000 companies at the time. Although that figure exceeds Dice’s recruitment package customer count, we note that Vettery had a freemium model in which companies paid nothing upfront and revenue was dependent on successful job placements. Thus, the more relevant metric, in our opinion, was that Vettery had 20,000 candidates on its platform at the time, which was viewed as a potential revenue opportunity approaching $400 million, and Adecco in effect paid $5,000 per candidate. We therefore surmise that an acquirer could take a small percentage of the 4.6 million active members on Dice and assume similar levels of monetization potential to validate a substantial revenue opportunity, and from there, apply a multiple akin to the per-candidate price paid by Adecco to justify an equity value well in excess of current levels.

All things considered, we are initiating coverage of DHI Group with a price target of $8.00, which represents a FY ’22 EV/Sales multiple just over 3x and an EV/EBITDA multiple of approximately 15x. We think our price target may well be just a pit stop en route to a more SaaS-like valuation, but we are opting for a more conservative approach at present given the relatively recent return to revenue growth. As the company demonstrates sustained growth in FY ’22 and beyond and exhibits progress towards its long-term margin targets, we will revisit whether a higher target multiple is in order.

Our report with model and disclosure is available here.

Disclosure(s):

K. Liu & Company LLC (“the firm”) receives or intends to seek compensation from the companies covered in its research reports. The firm has received compensation from DHI Group, Inc. (DHX) in the past 12 months for “Sponsored Research.”

Sponsored Research produced by the firm is paid for by the subject company in the form of an initial retainer and a recurring monthly fee. The analysis and recommendations in our Sponsored Research reports are derived from the same process and methodologies utilized in all of our research reports whether sponsored or not. The subject company does not review any aspect of our Sponsored Research reports prior to publication.